TUAC NEWS

OECD Economic Outlook: further downward revisions in growth forecasts

25/11/2013

OECD Economic Outlook: further downward revisions in growth forecasts

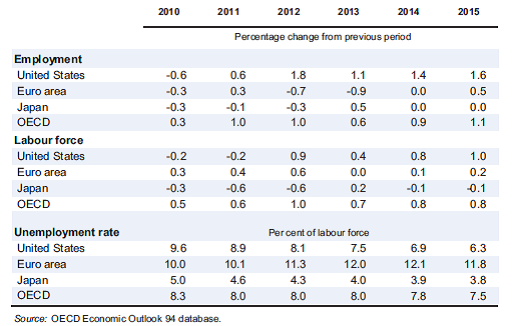

The past seven forecasts for growth from the OECD and indeed the IMF have all been successively revised downwards as austerity policies continue to bite in Europe and growth slows in the emerging economies. According to the latest OECD Economic Outlook, issued on November 19, the global recovery remains modest and uneven, with a continuing divergence in economic activity both between and within advanced and emerging economies. The forecast for global GDP growth has been revised down by just under ½ percentage point both this year and in 2014 to 2.7% and 3.6% respectively. Almost all of this reflects a further growth slowdown in the large emerging market economies (EMEs), which is tempering the pace of the recovery in the OECD economies.

Growth in the United States is projected at a 2.9% rate in 2014 and a 3.4% rate in 2015. In Japan, GDP is expected to drop to a 1.5% growth rate in 2014 and a 1% rate in 2015. The euro area is expected to witness a gradual recovery, with growth of 1% in 2014 and 1.6% in 2015. Due to the sluggish recovery stubbornly high unemployment, particularly in Europe, has been stable at a high level of 8.0%. It is not expected to drop significantly over the short and medium term. Provided the existing and large downside risks do not materialise, the average unemployment rate across the OECD might declining by about a ½ percentage point over the two years to 7.4% until the end-2015 while in Europe unemployment is only expected to fall below 12% by the end of 2015.

The OECD emphasizes that economic policies need to provide support to demand. However, the call upon advanced and emerging market economies alike, to commit to bold and ambitious structural reform policies is unlikely to bring down high unemployment. Structural reforms can be contractionary in the short term, if they increase perceived income insecurity and precautionary savings. Reducing the generosity of unemployment income support can also have negative short-run effects in “bad times”, i.e. when output and employment are substantially below potential. Moreover, job protection reforms can increase lay-offs quicker than they can boost job creation and thereby result in temporarily higher unemployment. Structural reform policies have also found to contribute to widening wage disparities and thus to an increase in inequality.

To read more, see https://www.oecd.org/economy/economicoutlook.htm