TUAC NEWS

A message for the world’s leaders at Davos: Mind deflation, (re)build stronger collective bargaining systems

20/01/2016

- 1601t_IMF_WEFpdf

Download the report on the right-hand side

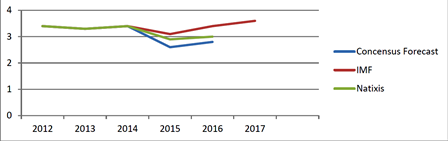

The IMF released its latest World Economic Outlook

(WEO) Update yesterday pointing to persistently weak growth and

another downward revision of its projected growth rates for 2016

and 2017 by 0.2 percentage points each year (

http://www.imf.org/external/pubs/ft/survey/so/2016/RES011916A.htm

). Despite this, the IMF’s growth trajectory still sees the world

economy recovering slightly from the weakness it experienced last

year (see Graph 1).

Graph 1: Outlook for world economic growth

Source: IMF World Economic Outlook Update (

http://www.imf.org/external/pubs/ft/weo/2015/update/02/pdf/0715.pdf

) and Natixis Flash Economie, 6/1/2016, nr. 20, (http://cib.natixis.com/flushdoc.aspx?id=88827

)

From past experience, however, we know that forecasters tend to

underestimate economic downturns while overestimating the recovery.

Given the vast list of negative shocks and developments that are or

will be hitting the economy, this time may NOT be different:

- In the US, the labour market is not in brilliant shape (unemployment numbers are low but the participation rate has fallen, there is no or little sign of accelerating wage dynamics either). At the same time, its economy is in its sixth year of economic expansion, a timing that is usually linked to the turning of the business cycle. The Fed’s decision to start raising interest rates in December 2015 would point in the same direction of a weakening business cycle (or rather one that is de facto being weakened because of monetary policy slowing it down).

- In the UK, growth over the recent years has been driven by household expenditure, which in turn was based on the reappearance of a certain real estate bubble. At this moment, however, household demand for new mortgages is decelerating. If the renewed real estate bubble would come to a standstill or go into reverse, UK growth performance would suffer.

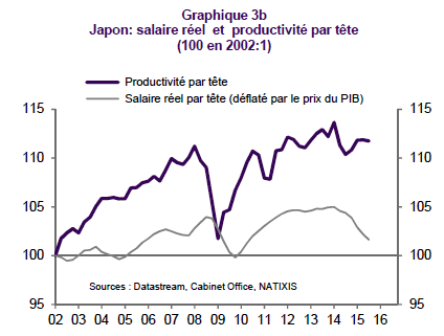

- In Japan, while ‘Abenomics’ is injecting short bursts of demand and growth into the economy, it is failing to kick start the process by which growth becomes self-sustained as real wages in Japan keep lagging behind productivity (see Graph 2). Even if the government seems to have rediscovered the value of coordinated collective bargaining in steering the economy away from deflation and in redistributing high but idle corporate cash reserves back to workers, too many jobs in Japan remain precarious, part time and hence underpaid.

Graph 2: Evolution of real wages and productivity per head in Japan since 2002

Source: Natixis, Flash Economie, 06/01/2016

- Meanwhile, the Euro area keeps struggling with its own contradictions: The policy choice that Euro area policy makers made on replacing the missing instrument of currency devaluation by an internal devaluation of wages keeps feeding into disinflation. Combine this drive for downwards wage flexibility with other factors such as headline inflation already at zero due to falling oil prices, inflation expectations back on a downwards trend, record high levels of (public but also private!) debt loads, piles of non-performing loans in several parts of the euro area banking system and, last but not least, a Stability Pact or Fiscal Compact that keeps pushing several member states (notably Spain, France, Italy) into fiscal austerity, it becomes clear that the world economy cannot count on the Euro area economy to drive world economic growth. The opposite is the case: With a current account surplus approaching a level of 3.7% GDP, the Euro Area is subtracting even more demand and growth from the world economy than before (and more demand than China or Japan, recording a current account surplus of 3% and 3.3% respectively).

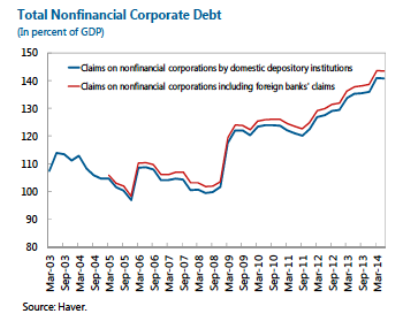

- In the emerging part of the world, China is caught in the same

trap of capitalist exuberance, over-indebtedness and

over-investment that other economies have come to know so very

well. As can be seen from the graphs below, since 2008, corporate

(non-financial) sector debt has gone into overdrive, increasing

from around 100% to almost 150% of GDP.

Graph 3: Nonfinancial Corporate Debt in China

Source: IMF, Assessing China’s corporate sector vulnerabilities, WP

15/72, (https://www.imf.org/external/pubs/ft/wp/2015/wp1572.pdf

)

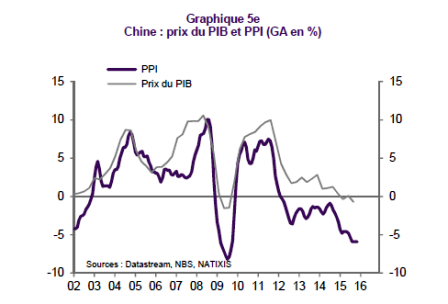

Sooner or later, however, over-investment results in overcapacity,

translating into downwards pressure on prices: Indeed, producer

prices in China (see PPI line in Graph 4) are now falling at a pace

of 5%. In addition to this, the exchange rate of the Chinese

currency is also coming under pressure so that the problem of

producer price deflation is not just limited to China but is also

exported to the rest of the world.

Graph 4: GDP deflator and Producer Price Index in China

Source: Natixis. Flash Economie, 06/01/2016

- The other big emerging economies (such as Brazil, South Africa) constitute the next domino. Their exports come under pressure as a result of weakening import demand from China for their commodities or from the competitive weakening of the Chinese currency. And, while the financial market turmoil that accompanies this will push the exchange rate of these economies further down, it will also result in higher interest rates (monetary policy becoming restrictive in an attempt to keep financial capital inside the country so as to limit the downfall of the currency), which will then stifle overall economic growth.

Two reflections going forward

1. The IMF itself, at least

implicitly, recognizes part of the concerns mentioned above as it

writes that risks are ‘tilted to the downside’. The IMF in

particular identifies these as ‘a generalised slowdown in emerging

markets, China’s rebalancing, lower commodity prices, and the

gradual exit from extraordinarily accommodative monetary conditions

in the US”.

2.

While at Davos, the world government and business leaders will

discuss the ‘future of work’- it is also important to look at the

‘present state of work’. Judging from the above, one cannot ignore

that the world economy is heading for another cycle of weakening

growth and this, at the very moment, when price and inflationary

pressures are already at too low levels. If, as it has been the

case in the past, this new slowdown would trigger a further

deceleration of inflation dynamics, too low inflation will become

outright deflation with all of its dire consequences on the economy

(rising real interest rates, increased real burden of debt, falling

aggregate demand, and ultimately, even more intense

deflation). In that case, policy makers would do well to consider

that strong and robust systems of collective bargaining do not only

tend to control for rising inequalities (as evidenced by a recent

IMF report https://www.imf.org/external/pubs/ft/sdn/2015/sdn1514.pdf

) but that, by keeping the level and dynamics of nominal wages up,

they can also play a key role in breaking the vicious circle

whereby falling prices and falling wages are chasing each

other.

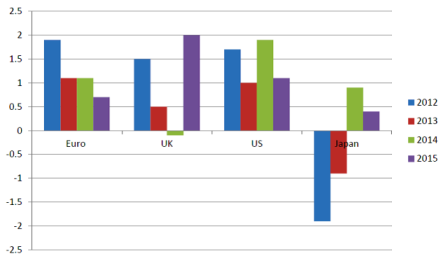

To illustrate the latter, consider Graph 5 showing that unit labour

cost dynamics have become particularly compressed and, especially

so in the case of Japan and the Euro Area, are way out of line with

minimal inflation targets of 2 or between 2 and 3%. The conclusion

to draw is straightforward: If central bankers want to steer the

economy away from the edge of deflation and revive modest inflation

rates, they would do well to start considering strong and

coordinated systems of collective bargaining as a way to uphold

price stability and re-anchor inflation expectations.

Graph 5: Nominal unit wage costs, annual percentage increase

Source: European Commission, 2015