TUAC NEWS

OECD WANTS HIGHER PUBLIC INVESTMENT AND HIGHER WAGES TO SUPPORT THE RECOVERY

01/06/2016

The economic forecasts the OECD released today are not painting a bright picture (http://www.oecd.org/eco/economicoutlook.htm ). While advanced economies would continue to grow, the OECD is expecting the pace of growth to remain disappointingly weak. After struggling to reach only 2% on average per year, OECD growth will now dive back down below 2% in 2016 and barely recover to 2.2% in 2017. While the Euro Area and even more so Japan are the (usual) laggards (respectively 1.5% and 0.6% growth for 2016), growth in the US (1.8%) is not so brilliant either. In other words, eight years after the crisis, the growth engine is far from being ignited and the economy continues to perform below its potential.

In analysing the causes and the remedies for dismal growth performance, the OECD’s Economic Outlook delivers a series of messages that are surprising and worth stressing.

Key policy channels have broken down

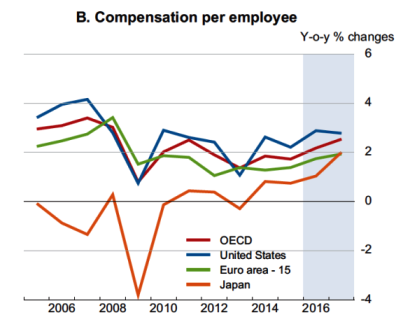

First, the OECD signals that the link between low (in some cases even zero) interest rates and investment has broken down. It offers a ‘Keynesian’ /demand side view for this by saying that “if companies continue to doubt that national and global demand will strengthen (…), business investment growth will be weaker than projected”.Even more surprising is the OECD’s explicit reference to the role of muted wage gains in keeping the upturn modest. Indeed, as can be seen from the graph below, while nominal wage growth has come down since the crisis, it has failed to recover since then.

What can also be seen is that the OECD’s forecast is actually based on the assumption that wages will strengthen in 2017, thereby giving more support to recovery. As the OECD argues in its text, “if the links (between lower unemployment and wage growth) were to be even weaker than assumed, the pick-up in growth would be slower”.

In other words, it seems as if the OECD is now implicitly acknowledging that wages are not to be seen as a cost factor but as an engine for demand and recovery.

The ‘low growth trap and how to escape from it

The OECD continues to surprise by warning that the weak recovery has led to a ‘low growth trap’, a trap which has nothing to do with globalisation or technological or demographic changes but with years of dismal growth performance resulting in a self- fulfilling prophecy. Investment is weak because business is expecting low demand and demand is low because business is not investing. At the same time, the lack of investment is eroding the capital stock and preventing new innovations from spreading throughout the economy. So when policy makers (including the OECD itself) are concerned about productivity slowing down, a major part of this slowdown can actually be explained by the failure of macro - economic demand management in ensuring complete recovery from the financial crisis.If however (and note that this is again the language of the OECD) a different growth path is taken, with faster wage growth together with greater equity, then higher demand will lead to higher investment, higher productivity and more innovation as businesses invest in new products, new processes and new workplaces.

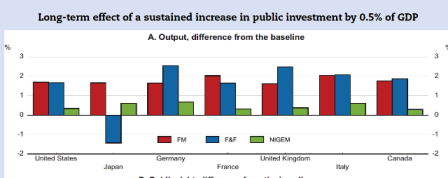

To shift our economies to such a path, the OECD insists on the role of active fiscal policy. Monetary policy, already overburdened, should remain supportive of the economy but can’t do much more. Fiscal policy should now be deployed more extensively and, by locking in very long interest rates at long maturities, also has the fiscal space to do so. This call for a fiscal stimulus is backed up by simulations showing high multipliers for public investment expenditure. If public investment is increased by 0.5% of GDP, economic activity goes up by around 0.4%, even 0.6% in case the public investment push would be coordinated amongst the OECD economies. The next graph describes the results from three different models, with all three of these showing positive results for the economy (except in one model for Japan).

There is also the improved sustainability of public finances that according to the OECD will result from the stimulus: The increase in economic activity will lower the ratio of public debt to nominal GDP by increasing the latter (the denominator effect).

Structural reforms: Stop digging an even deeper hole

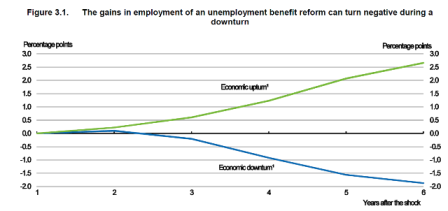

While the proposal for a public investment stimulus is linked with the usual language of structural reforms, the OECD’s outlook is at the same time suggesting taking a more nuanced approach. This reflects research published in an earlier OECD publication finding that several structural reforms, when undertaken in a period of crisis and certainly when monetary policy is already near the zero bound on nominal interest rates, will deepen and prolong the crisis by further depressing demand (see here https://www.hse.ru/data/2016/03/06/1125706157/1216011e.pdf ). This is particular so in case of reforms that put downwards pressure on wages. It is also the case for reforms that cut unemployment benefits as such reforms will squeeze aggregate demand (unemployed lose benefits without gaining jobs as they are not available), thereby leading to a loss in employment and this even six years after the reform (see graph below).